How can you minimize financial stress during COVID-19?

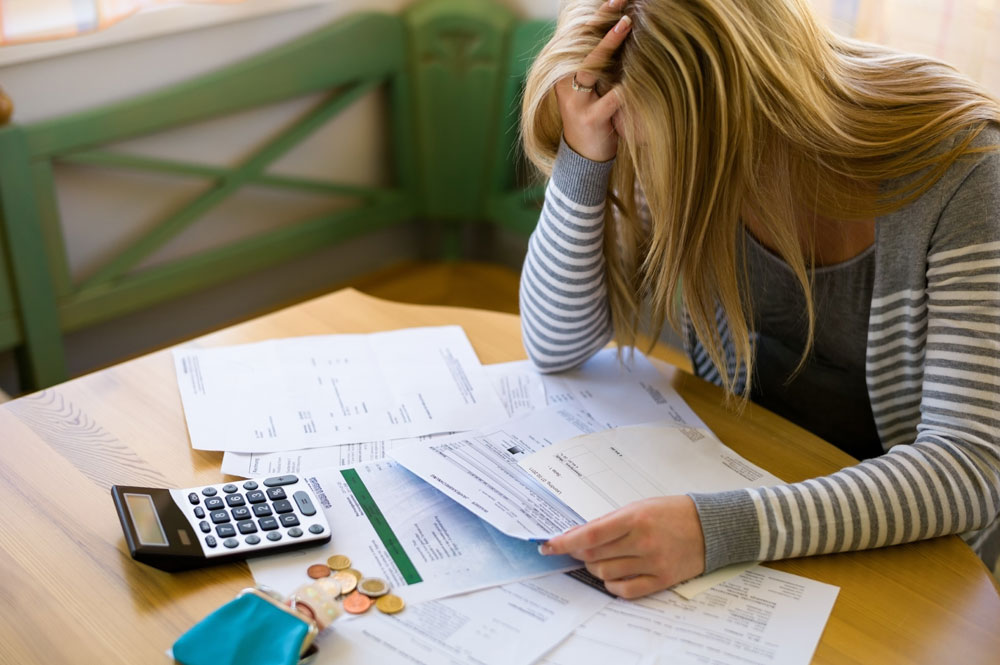

There is no doubt that Americans are dealing with financial stress as a result of the pandemic. Recent research has shown that the hardest-hit by the pandemic are low-income Americans and communities of color, but there is no doubt the anxiety of financial stress during COVID-19 is affecting all Americans of all races and income levels.

Even many families with cash reserves and “emergency cushions” are beginning to see their resources dwindle as the pandemic drags on into 2021.

In this article, you will learn:

- What you can do to minimize financial stress during COVID-19,

- Whether you are a low-income worker hard-hit by the pandemic or a middle-income American who is adjusting to the new reality of the pandemic.

Americans are Concerned About Financial Stress During COVID-19

Surveys conducted last year by the National Endowment for Financial Education (NEFE) reveal a number of alarming statistics about our nation’s financial health and the financial stress experienced by people of all income levels during COVID-19.

For example:

- About two in three adults are at least “somewhat concerned” about their financial situations during COVID-19, while one in three are “extremely/very concerned.”

- More than four in five Americans report stress related to their personal finances during the pandemic, including stress related to having enough money saved, paying their bills, paying down their debt, income fluctuations, and job security.

- More than four in five Americans report similar concerns about their financial stability over the next 12 months.

- Two in five adults believe that they will still feel financial stress caused by COVID-19 in 12 months, while just one in three believe that they will feel “very/somewhat optimistic.”

- Three in four have made financial adjustments due to COVID, two in five have cut their monthly expenses, and one in four report putting off major financial decisions.

- Two in five report that they have provided financial assistance to family or friends due to COVID-19.

- 84% of those who provided financial assistance to friends or family say that it has caused some strain on their own finances.

- One in three report having received financial assistance from friends or family during the pandemic.

What Can You Do to Minimize Financial Stress During COVID-19?

The bottom line is that a majority of Americans are reporting some financial stress caused by COVID-19, but what can you do to minimize that stress?

1. Make a Budget

You may already have a budget, but it may need to be stripped down to the essentials if you haven’t already done so.

Just to get over the hump, you may need to reconsider budget items like:

- Subscription services: goods and supplies that you pay a monthly premium for that are not necessary, like pre-prepared meals, mystery clothing, or “shave clubs.”

- Restaurants: many people don’t realize just how much they spend on take-out and restaurants over the course of a month. Consider a “moratorium on eating out” until things start looking up again.

- Groceries: Most people can cut their grocery bill significantly by switching to generic foods and cutting out the non-essential grocery items like that second jumbo box of nutty-buddy bars.

- Entertainment: you may be able to cut expenses by letting go of some streaming services like HBO or other premium channels, by switching to a lower-cost cable alternative like Philo or Sling, or by cutting out cable television altogether.

The idea is, if it’s discretionary, you can let it go, temporarily, until you are feeling more financially secure. What about things that are not discretionary, though, like your mortgage and utility bills?

2. Negotiate Your Bills

Trying to cut back on your expenses can be frustrating, because some of those expenses just aren’t optional. You may be surprised at the results you can get if you call your bank, your credit card companies, or other lenders and ask if there is anything they can do to help.

For example:

- Mortgages and rent payments: your bank, lender, or landlord may be willing to defer payments, modify your payment plan, or they may have other options that are available. There may be a moratorium in place for evictions, financial aid for landlords, or other government-imposed protections that are available as well. You can find a state-by-state breakdown of current programs on HUD’s website.

- Credit cards: many credit card companies have assistance that is available in the form of payment deferrals, waiver of interest, waiver of fees, and extending payment due dates.

- Student loans: there are options available for help on student loan payments as well, including income-driven repayment (IDR) plans, deferments, and forbearances.

3. Look for Community Assistance Programs

There may be local governmental relief programs and local community programs that can provide some relief with:

- Utility payments,

- Mortgage payments,

- Meal assistance,

- Food banks,

- Grocery store assistance, or

- Transportation.

You can learn what resources are available in your area through government websites or by contacting churches, food banks, community centers, and local advocacy groups.

4. Utilize Available COVID-19 Relief Funds

Most Americans have received one or more COVID-19 stimulus checks, but there may be other resources that are available through COVID-19 relief bills passed by Congress.

For example, if you have a small business – even if it is a small, one-person operation – there may be funds available through Paycheck Protection Program (PPP) loans that can be forgiven if you qualify.

5. Take Advantage of Free Resources for Financial Planning

One way to minimize financial stress during COVID-19 is to take advantage of the many free or low-cost resources that are available for financial education, including:

- Smart About Money from the NEFE,

- The United Way, or

- The AARP.

6. Bankruptcy

In appropriate cases, bankruptcy can also provide relief and minimize the stress from COVID-19.

Depending on your circumstances and the type of bankruptcy that you file:

- Some of your debt may be erased;

- Your debts may be reorganized and a repayment plan set up; and

- Your assets are protected up to certain limits.

Considering bankruptcy in South Carolina?

If you’re considering bankruptcy and reside in South Carolina then bankruptcy attorney Michael Culler may be able to help. Please call (803) 536-5055 or use this contact form to send him an email.

Culler Law Firm serves all of South Carolina including but not limited to Orangeburg, Columbia, Charleston, and Mrytle Beach.

Ready To Speak With An Attorney?

Get your case evaluated by a real attorney at no cost to you.